Motorbike rental insurance Thailand has four tiers in 2026 and the rental shop only sells you the first two. Tier 1 (compulsory Por.Ror.Bor, included free in the daily rate) caps third-party medical at 30,000-80,000 THB and pays nothing toward your bike or your hospital bill. Tier 2 (basic damage waiver, 100-200 THB/day) covers your rental bike with a 20,000 THB excess. Tier 3 (mid-tier, 200-400 THB/day) drops the excess to 10,000 THB and adds theft cover. Tier 4 (comprehensive plus, 300-700 THB/day) drops the excess to 5,000 THB. None of these tiers covers your own injuries; that gap belongs to your travel insurance, which is a separate purchase from a separate provider.

Key Takeaways

- Shop CDW typical: most rental shops include Por.Ror.Bor (free) and sell a basic damage waiver at 100-200 THB/day with a 20,000 THB excess. "Insurance included" almost always means just Por.Ror.Bor.

- Travel insurance covers what the shop won't: your medical evacuation, surgery, and hospital stay. Shop CDW covers the bike. The two products don't overlap.

- Excess (deductible) norms: 5,000-20,000 THB per incident, scaled inversely to the daily fee. A 100 THB/day waiver typically carries the highest 20,000 THB excess.

- Exclusion list that voids every tier: no IDP-with-motorcycle endorsement, alcohol or drugs, off-road or unsealed surfaces, named-driver-only policy, racing, more than one pillion.

- Claim timeline: 2-4 weeks for an undisputed shop-CDW bike-damage claim if you have the police report and pre-ride video; 6+ months once liability is contested.

- Deposits: 500-5,000 THB cash is the legitimate Thai range. Original passport as deposit is a red flag, not a standard practice.

What rental shops actually include in the daily rate

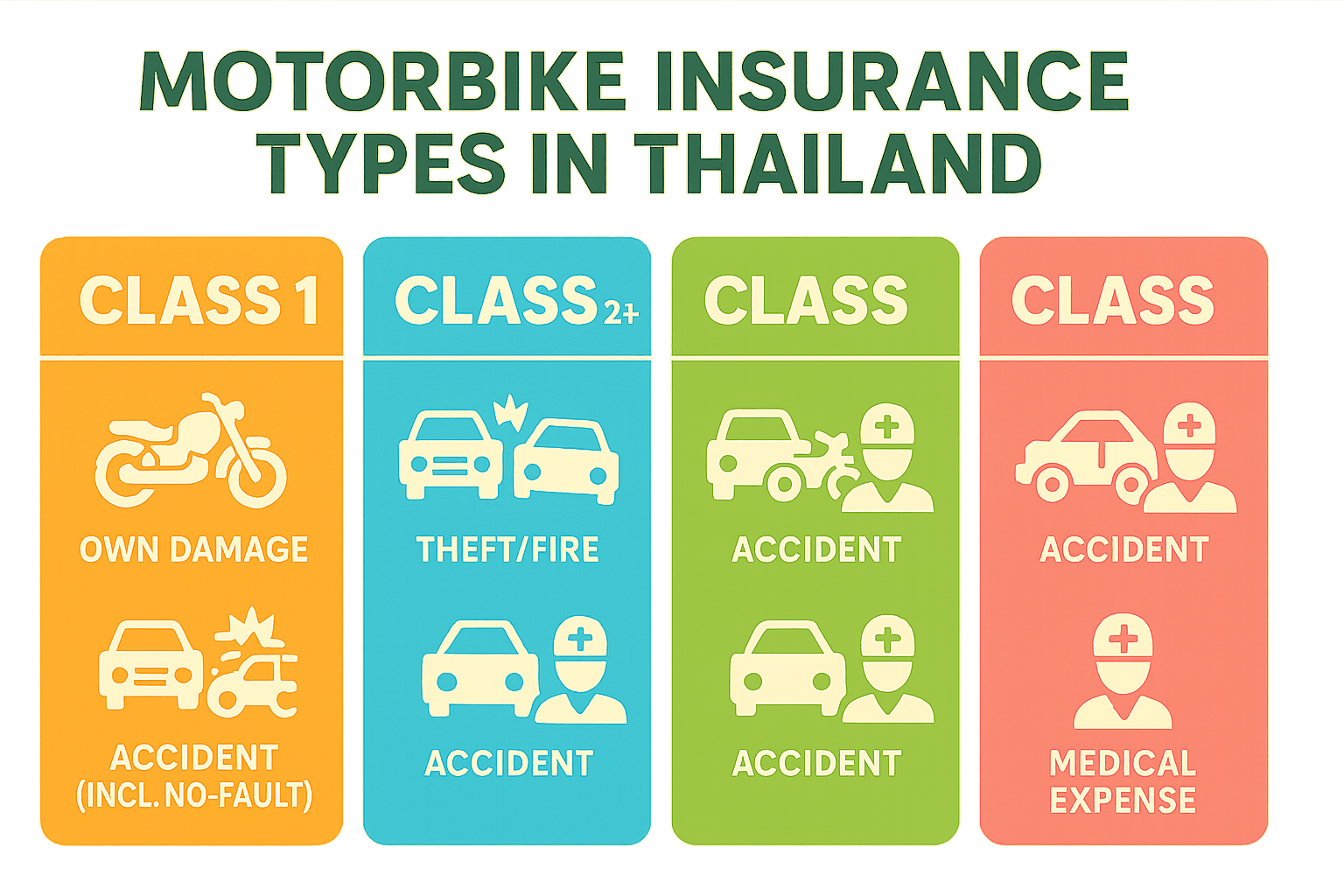

Thai rental shops bundle Por.Ror.Bor (พ.ร.บ.) into every daily rate by default because Thai law requires it on every registered bike. The compulsory third-party scheme is administered by Road Victims Protection Co., Ltd. (RVP), the industry pool that pays out the third-party medical claims. That bundle covers third parties you injure, up to a 30,000 THB without-fault cap and 80,000 THB once fault is established. It does not cover you, your bike, your pillion if you caused the crash, the parked car you scraped, or the rental shop's repair bill. When a shop says "insurance included" or "fully insured", they almost always mean this single layer. Anything beyond Por.Ror.Bor is an upsell, sold by the day at the counter or, increasingly, at booking time on platforms like Byklo.

The damage waiver is the layer that matters for the rental transaction. Shops sell it under several names (CDW, "damage waiver", "bike protection", "Type 1 daily") but the structure is the same: the shop fronts the repair cost and you pay the excess plus any exclusion. The basic Tier 2 waiver is the most common upsell at street rental counters, priced at 100-200 THB/day on a 125cc Click and 200-400 THB/day on a 250-400cc manual or 650cc big bike. Coverage scope: damage to the bike from a crash you caused, with a 20,000 THB excess that you pay first. The Thai Department of Land Transport publishes the official Por.Ror.Bor framework for verification of the compulsory layer.

Theft cover is rarely bundled into the cheapest waiver. If a shop sells "theft included" at 100 THB/day, read the contract: most cap reimbursement at 50% of the bike's value or exclude theft entirely if you didn't have keys on you at the moment of theft. Premium Tier 3 and Tier 4 waivers (200-700 THB/day) add proper theft cover with a 5,000-10,000 THB excess. The Thailand Motorbike Rental Scams Guide covers the staged-theft pattern that exploits weak theft policies.

What travel insurance covers that the shop will not

Travel insurance is a separate product from a separate provider, and it covers a different category of loss. The shop's damage waiver pays for the bike. Your travel insurance pays for the broken collarbone, the 5-day hospital stay, the medical evacuation home, and the lost-luggage claim if your panniers vanished in the crash. The two products do not overlap, and you need both for genuine protection. The financial timeline of a serious crash, broken down hour by hour, is covered in the dedicated H2 below.

The single biggest blind spot is engine size. Standard travel insurance from a major underwriter or your premium credit card almost always either excludes motorbikes entirely or caps the engine size at 50cc. Thai rental fleets start at 110cc; a Honda Click 125, a Yamaha Filano, a Yamaha NMAX 155, and every PCX model are all on the wrong side of that 50cc line. Without an explicit "motorcycle" rider that names 125cc or higher, your travel policy denies the claim the moment you sit on the rental.

The license clause is the second blind spot. Travel insurance contracts include an "illegal act" exclusion: any claim arising from an unlawful act at the time of accident is denied. In Thailand, the unlawful acts that trigger denial include riding on a car-only IDP, no IDP at all, no helmet, or alcohol over the legal limit. The fine at a Thai checkpoint for missing IDP is 500-1,000 THB on the spot, but the bigger consequence is that the same evidence makes any subsequent travel-insurance claim a guaranteed denial. The International Driving License Thailand post walks through the IDP application.

How a real accident plays out: the financial timeline

The medical-cost data isn't hypothetical. Thailand has one of the highest road-accident rates in the world (see WHO road-traffic injury statistics for the global comparison), and motorbikes account for the majority of serious injuries among foreign tourists. The ExpatDen breakdown of Thai motorbike insurance walks through the cost structure post-by-post. The financial timeline of a typical foreigner-rider crash in 2026 looks like this:

- The first hour at the ER: 5,000-15,000 THB ($140-425 USD) for a trauma assessment, X-rays, and basic wound care. Por.Ror.Bor often covers this fully if your fault status is clear.

- The first surgery (broken bone, pin insertion, basic orthopedic): 100,000-300,000 THB ($2,800-8,500 USD) at a Thai private hospital. Por.Ror.Bor's 30,000-80,000 THB cap is exhausted; the gap falls to you or your travel insurer.

- A 5-7 day hospital stay: another 50,000-150,000 THB depending on private-room class. Almost entirely on you without travel insurance.

- Medical evacuation home: $25,000-100,000 USD for an air ambulance to a Western country. Travel insurance with med-evac is the only realistic way to fund this.

- Months of rehabilitation and follow-up surgery at home: variable, but commonly $30,000-80,000 USD total. Your home health insurance, with the gaps filled by the travel insurer if your policy has post-trip provisions.

A single bad scooter crash on a rented Honda Click (the most common rental bike in Thailand) can hit a $100,000+ USD lifetime cost without proper coverage. The annual GoFundMe campaigns for stranded tourists in Phuket and Pattaya hospitals are not exotic edge cases; they're the predictable outcome of riding without proper travel cover.

Where the gap is: what neither product pays

Between the shop's damage waiver and your travel insurance, three categories of loss commonly fall into the gap. First, the excess on the shop CDW. A Tier 2 waiver leaves you personally liable for the first 20,000 THB of any bike-damage claim. Travel insurance does not pay this gap; it covers your medical bill, not the shop's repair invoice. Second, anything excluded from the waiver: off-road riding, unsealed surfaces (the dirt road to a waterfall), alcohol over the limit, more than one pillion, named-driver-only policy where your friend rode the bike, or a missing IDP. Third, the policy's coverage cap.

The named-driver clause catches more renters than any other exclusion. Most rental contracts list a single named driver, and the named-driver-only waiver voids if anyone else rides. A common scenario: two friends rent one bike, swap as drivers across a weekend, and the second driver crashes. The shop charges full repair cost (not just the excess) because the named driver wasn't behind the wheel. The fix is to add a second named driver at booking, usually for an extra 50-100 THB/day, or to rent two separate bikes.

The off-road exclusion catches travelers who don't realize they've left a sealed road. The Pai Loop on Route 1095 is paved; the loose-gravel detour to a hot spring is not. The road to Bua Tong Sticky Waterfall is paved; the last 200m is rutted dirt. If you crash on the unsealed section, your damage waiver may exclude the claim and your travel insurance may treat the surface as "off-road riding" for exclusion purposes too. Specific routes and bike-class recommendations are in the Motorbike Rental Checklist Thailand.

The third gap is the deposit. Most Thai shops hold 500-5,000 THB in cash as a deposit; some street shops in Phuket and Pattaya demand 10,000+ THB or the original passport. The deposit secures the bike against minor damage that wouldn't trigger a waiver claim (a scratched mirror, a cracked plastic panel). The shop deducts repair costs from the deposit before refunding it, and the repair cost is determined by the shop's mechanic, often at 2-3x market rates. Photos and a 30-second pre-ride video are the only effective defense against an inflated deduction.

How rental tiers compare in 2026

The pricing scales inversely to the excess: cheap waivers carry high excess, premium waivers carry low excess. On a one-week 125cc Click rental, the math works out roughly even between Tier 2 (1,400 THB/week with 20,000 THB excess) and Tier 4 (4,900 THB/week with 5,000 THB excess) once you weigh the probability of a claim. Riders under 25, first-time scooter renters, and anyone planning a Mae Hong Son Loop or Pai Loop run should bias toward Tier 4. City-only riders on flat sealed roads can reasonably take Tier 2 with a strong pre-ride video.

For the daily rate context, 125cc rentals across Thailand sit at 150-350 THB/day in 2026 per the Thailand scooter rental cost breakdown. A 100-200 THB Tier 2 waiver effectively doubles the headline rate, which is why the upsell pressure at street rental counters is so visible. Booking through a vetted platform usually displays the waiver and excess directly in the listing rather than at the counter. (For context on owned bikes, annual Class 1 premiums in 2026 run 3,500-7,000 THB depending on the bike's engine class and the rider's history, which is why the daily Tier 3-4 add-ons are priced where they are.)

What a real rental insurance claim looks like

A typical bike-damage claim plays out across the rental shop, the police, and the insurer; the timeline depends on whether liability is contested. The clean case: a solo rider drops a 125cc Click on a wet Phuket curve, totaling the front fairing and bending the brake lever. No third party involved. Repair quote at the shop: 18,000 THB. Tier 2 waiver in effect with a 20,000 THB excess. The waiver pays nothing; the renter pays the full 18,000 THB to the shop because it is below the excess. The waiver "kicks in" only above 20,000 THB.

The contested case: same rider, same crash, but with a Thai car driver involved. Police arrive, write a report, assign fault. If the rider is at fault and on a Tier 2 waiver, the renter pays the first 20,000 THB excess plus any third-party property damage above the Por.Ror.Bor cap. If the Thai driver is at fault, the renter's insurer pursues the Thai driver's policy. Settlement timeline: 2-4 weeks for an uncontested claim with a clean police report; 6+ months once fault is genuinely contested. Bring the pre-ride video and the rental contract to the shop the same day to get the claim opened.

The denied case: the rider lacked an IDP-with-motorcycle endorsement, or had a positive breath test, or the shop later proves the rider was off the sealed road. Every tier denies the claim. The renter pays 100% of repair cost, plus any third-party damage out of pocket, plus the police fine. Travel insurance also denies the medical claim under the same illegal-act clause. This is the financial nightmare scenario that makes IDP and zero-alcohol non-negotiable.

A practical tip on third-party scenarios: even when you're at fault, the renter's exposure for property damage (the Mercedes you scraped, the somtam cart you flattened) is usually capped by Por.Ror.Bor's third-party-property layer or by the Tier 3+ third-party coverage. The exposure that matters is medical, and medical exposure scales fast: a Thai private hospital surgery for the OTHER party can hit 100,000-300,000 THB, and Por.Ror.Bor's 30,000-80,000 THB cap leaves you on the hook for the gap if the third-party didn't carry their own cover. Tier 3 and Tier 4 waivers usually extend third-party medical coverage to 1,000,000 THB, which is the meaningful upgrade for anyone riding in dense urban traffic in Bangkok or Pattaya.

How to verify the policy before you sign

The shop counter is the wrong place to read a contract for the first time. Three checks shift the odds materially: ask for the policy in English (in writing, not verbally), confirm the excess and named-driver scope, and verify Por.Ror.Bor is current. Most reputable shops will hand over a one-page English summary of the waiver terms; street shops that resist this question are sending a signal worth heeding.

The Por.Ror.Bor verification is a 10-second job and prevents one of the cleanest preventable disasters. Look at the bike's tax sticker (the small square sticker on the front fork or under the seat showing the year of road tax). If the sticker is current year, Por.Ror.Bor is paid and the bike is road-legal. If the sticker is missing or expired, the bike is operating illegally; any accident voids every tier including travel insurance, because riding an unregistered bike is itself an illegal act.

The named-driver question is asked in two parts. First: is the policy named-driver-only or does it cover any licensed rider with an IDP? Second: if I add a second driver, what does it cost? Adding a named driver is usually 50-100 THB/day. Skipping the question is one of the most expensive mistakes a two-rider couple can make. The same logic applies to the geographical scope: most policies are nationwide, but a few cap to the rental city's province; the question costs nothing to ask.

The list of documents to demand before paying: the written rental agreement (with deposit type, fuel policy, damage liability, and waiver tier in print), the policy summary in English, and a photo of the tax sticker. The Motorbike Rental Checklist Thailand covers the full pre-ride procedure including helmet check and brake test.

Pre-ride safety check (5 minutes)

Insurance pays for the broken leg; a properly-maintained bike with proper documentation prevents the leg from breaking in the first place. The mechanical-safety checklist below complements the policy verification above; running it takes 5 minutes and shifts the odds materially before you turn the key.

- Tires: visible tread, no bald patches. Bald tires lose grip in the first rainfall and on the loose sand that drifts across coastal roads.

- Brakes: both levers should bite firmly without touching the handlebar. Worn pads or a stretched cable are common in cheap rentals.

- Lights: headlight high and low beam, both indicators, brake light. Thai law requires headlights on day and night.

- Helmet: proper full-face or three-quarter; "soup bowl" half-shells are legally compliant but functionally useless. Both rider and pillion mandatory under Thai law.

- Pre-ride video walkaround: 30 seconds documenting every existing scratch. Stops the scratch-fee scam and gives you evidence in any insurance dispute.

The shop's track record is its own form of insurance. Vetted partner networks screen for shops that maintain bikes properly and run transparent rental contracts; the alternative is to walk into a Bangla Road or Beach Road street shop and gamble on whether the bike has had its brake pads changed in the last year.

Frequently Asked Questions

What's the difference between rental shop insurance and travel insurance?

Rental shop insurance covers the bike (damage, theft, third-party property). Travel insurance covers the rider (medical, evacuation, repatriation). The two products do not overlap and you need both. Shop insurance is sold at the counter or at booking; travel insurance is bought from a major underwriter before you fly, with an explicit motorcycle rider that names 125cc or higher.

Does my home-country travel insurance cover a Thai rental scooter?

Almost never by default. Standard travel policies either exclude motorbikes entirely or cap the engine size at 50cc, while Thai rental fleets start at 110cc. You need a policy with an explicit "motorcycle" or "adventure sports" rider that names 125cc or higher, plus operator (not just passenger) coverage. Read the fine print before you fly; verify with your insurer in writing.

What is the typical excess on a Thai rental damage waiver?

5,000-20,000 THB per incident, scaled inversely to the daily fee. A 100-200 THB/day basic waiver carries a 20,000 THB excess. A 200-400 THB/day mid-tier drops the excess to 10,000 THB. A 300-700 THB/day comprehensive-plus drops it to 5,000 THB. The excess applies per incident, so multiple claims trigger multiple excess payments. Verify the excess in writing before paying.

Will the shop charge me for a tiny scratch when I return the bike?

If the scratch isn't documented in the pre-ride video, often yes. Most shops inspect on return and deduct repair costs from your cash deposit at their mechanic's quote, which typically runs 2-3x market rates. The 30-second pre-ride walkaround video on your phone is the cheapest defense: every existing imperfection becomes documented prior damage rather than a chargeable new mark.

What happens if I crash without an IDP?

Every tier of insurance denies the claim. Riding without an IDP-with-motorcycle endorsement is an illegal act under Thai law; the shop's damage waiver, the Por.Ror.Bor third-party cover, and your travel insurance all reference the illegal-act clause. You pay 100% of the bike repair, all third-party damage, all medical bills, plus a 500-1,000 THB police fine. The IDP is the cheapest insurance you can carry; AAA and the UK Post Office both issue them in days.

Do I need an International Driving Permit (IDP) to rent a scooter in Thailand?

Yes, if you're a non-ASEAN tourist. Thai law requires the IDP-with-motorcycle-endorsement combination paired with your home-country motorcycle license. Without it, police checkpoint fines run 500-1,000 THB AND your travel insurance is voided in any subsequent accident. The International Driving License Thailand post walks through the 6-step IDP application.

Will my insurance pay out if the accident wasn't my fault?

Not automatically. Insurance contracts include an "illegal act" clause: if you were doing anything illegal at the moment of the crash (riding on a car-only license, no IDP, no helmet), the insurer denies the claim regardless of who caused the accident. A drunk Thai truck driver hits you head-on, but you were riding without an IDP, you get $0. The license documentation is your "get out of jail free" card for the insurance claim, not just a checkpoint dodge.

How long does a rental insurance claim take to settle?

A clean, uncontested bike-damage claim with a police report and pre-ride video settles in 2-4 weeks. Once liability is contested, claims can drag for 6 months or longer. File the police report within 24 hours of any incident, photograph the damage and the scene, keep all paperwork organized, and email everything to the shop the same day. Travel-insurance medical claims run on a separate track from the shop claim.

Should I use the shop's insurance or buy my own?

For the bike (shop CDW), the shop's policy is the only realistic option because it's tied to that specific bike's registration. For your medical (travel insurance), buy your own from a major underwriter before you fly; the shop does not sell rider-medical cover. The two products are complementary, not competitive.

Three pillars before you ride

A safe motorbike trip in Thailand stands on three pillars. Get them all right before keys change hands:

- Legal compliance: home-country motorcycle license + International Driving Permit with the "A" endorsement. The IDP turns checkpoint fines from a 500-1,000 THB hassle into a non-event AND keeps your insurance valid.

- Financial protection: Por.Ror.Bor (free, included), shop CDW on the bike (100-700 THB/day with 5,000-20,000 THB excess depending on tier), and travel insurance with explicit motorcycle rider, 125cc+ coverage, operator status, and medical evacuation. The travel insurance is the layer foreigners most often skip.

- Mechanical safety: a vetted, maintained bike with proper documentation. The 5-minute pre-ride check costs nothing and catches the failures that cause crashes.

Lock in the third pillar before you fly: browse vetted partner shops in 15 cities at Byklo.rent. The waiver tier and excess are surfaced in the listing rather than at the counter, helmets are included by default, and Por.Ror.Bor is verified at the shop level. If you're planning a city-base rental from Sukhumvit or Khao San, How to Rent a Motorbike in Bangkok covers the on-the-ground specifics.